Mr. Le Quang Trung, Deputy General Director of Vietnam National Shipping Lines, said that the shipping industry can recover in the third quarter, in which, the biggest catalyst comes from the Chinese market, when the country strengthens trade after the opening period. The market may recover in a V-shape. The second quarter will be the time to create a bottom.

The golden age is over

Table of Contents

The shipping industry seems to have passed the golden age period from 2021 to 2022 and gradually moved back to the Thai camp like before the COVID-19 pandemic.

The Freightos Baltic Index (FBX) global container shipping price index (FBX) as of May 12 was $1,437 per FEU (1 FEU corresponds to a 40-foot container), down from $9,280 in the same period last year. Prior to that, this index peaked at $11,109 in September 2021.

Global FBX Index from 2017 to 12/5/2023

FBX is a daily shipping container index issued by the Baltic Exchange and freight booking platform Freightos. The index measures global container freight rates by calculating spot prices for 40-foot containers across 12 global trade routes.

Compared to a year ago, freight rates from Asia to the US and Europe decreased by about 80%.

According to data from Drewry, the container freight rate (1 FEU) for the Shanghai-New York route as of May 11 was about $2,207, down from $11,264 a year earlier.

Or the freight from Shanghai to the city of Rotterdam (Netherlands) decreased at the same rate to $ 1,645.

In the period of 2021 – 2022, when the bottlenecks caused by the COVID-19 epidemic in the shipping industry are eliminated, the demand for transporting import and export goods of countries, especially China, increases dramatically. . Meanwhile, the supply of empty containers and ships is in short supply, causing freight rates to increase by the hour. The event that Ever Given’s giant cargo ship was stuck in the Suez Canal made the situation of freight rates more stressful when freight activities were congested.

The sudden increase in demand and while the supply has not been able to meet, Chinese customers, under the pressure of transporting their goods in accordance with the contract, have accepted the extremely high freight rates. For them, the fear of a contract penalty is bigger than the freight rate and more importantly, their inventory has been left for too long and has no room to store it. Therefore, shipping lines give priority to this market.

A representative of an enterprise in the logistics industry in Vietnam said, “We are also very shocked. In the morning, the freight rate from Vietnam to the US is 5,000 USD for 1 FEU, 7,000 USD in the afternoon, up to 15,000 USD at night. The level of increase that even we and those who have been in the profession for decades cannot imagine.”

But now everything has changed, fares have fallen deeply and gradually returned to pre-COVID-19 levels.

Talking to the writer, Mr. Le Quang Trung, Deputy General Director of Vietnam National Shipping Lines Corporation – JSC (VIMC, Code: MVN) said that the reduction in freight rates in the past period was due to many problems, in which The weakness comes from the reversal of supply and demand balance compared to the period of 2021 – 2022.

Specifically, import and export activities of many commodity sectors decreased by 30-50%. Meanwhile, during the period of hot freight rates, many carriers around the world invested in equipment, building new ships and containers.

“While the demand is decreasing, the new transport supply has been brought in on a large scale, creating a lot of downward pressure on prices. In addition, the reduction in freight rates is also due to seasonal problems, especially in the first quarter – the time of many holidays,” Trung said.

Mr. Le Quang Trung, Deputy General Director of Vietnam Maritime Corporation – JSC (Photo: H.My)

Profits of many businesses fell deeply

The reduced freight rates have clearly reflected in the business results of some shipping companies.

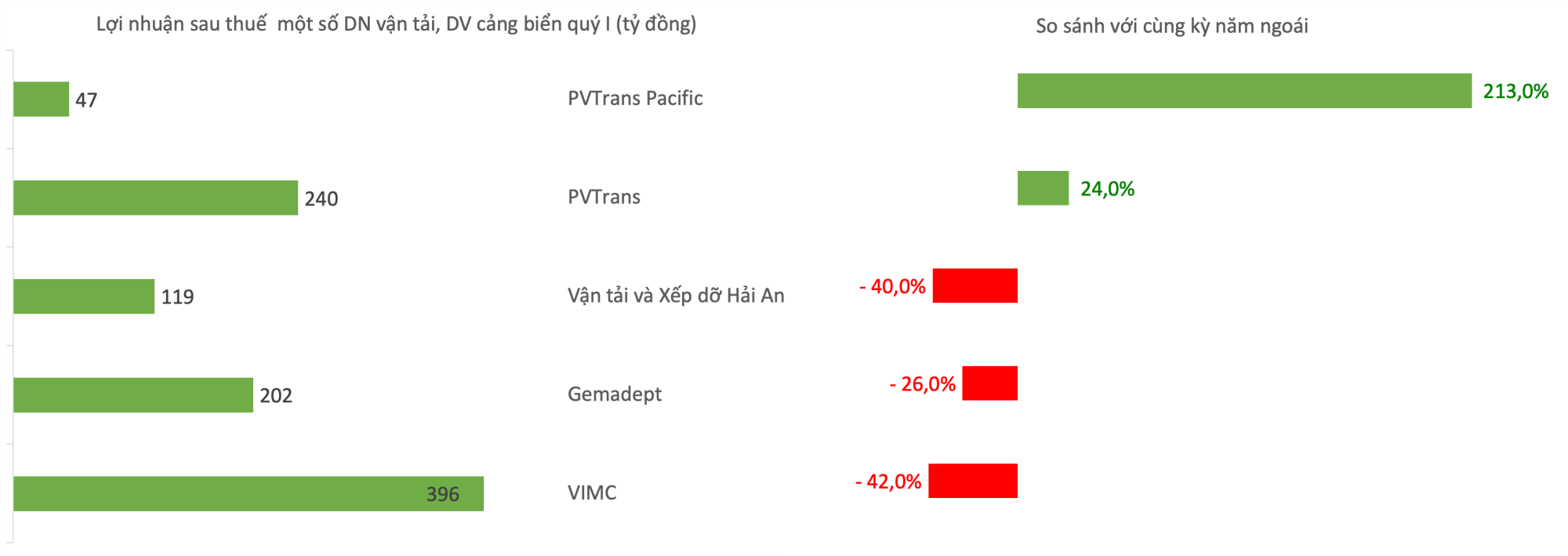

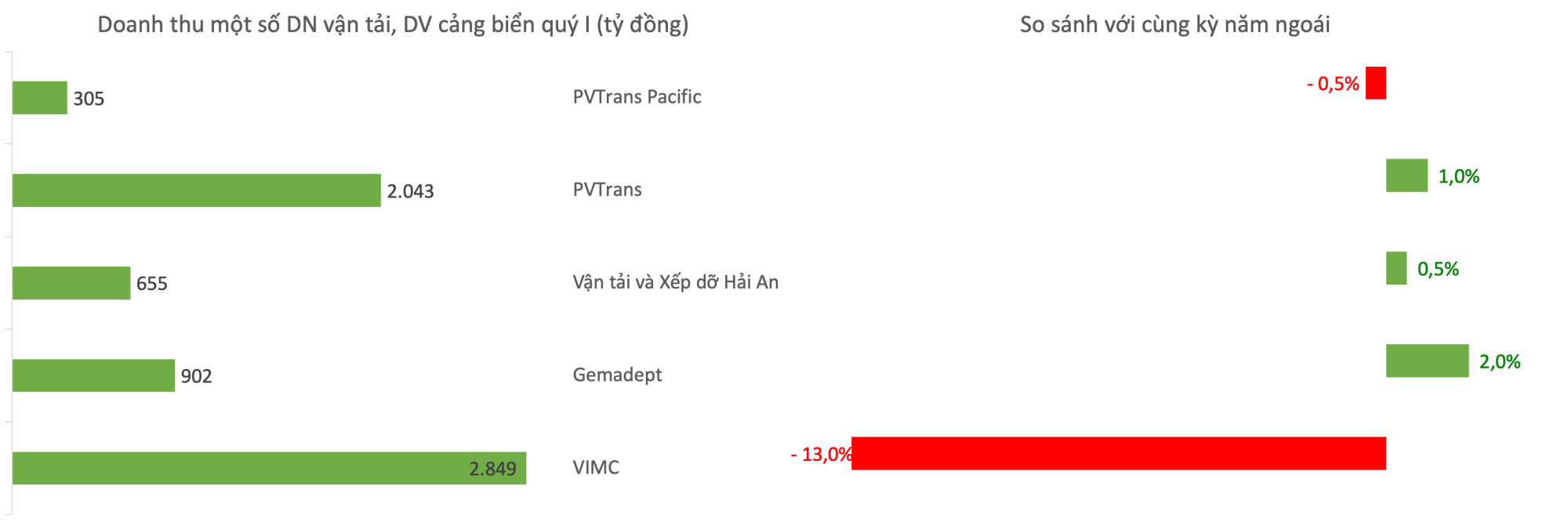

The consolidated financial statements for the first quarter of 2023 of Vietnam National Shipping Lines showed net revenue of VND2,849 billion, down nearly 13% over the same period. In which, transportation contributed VND 1,076 billion, port operation and cargo services contributed VND 1,451 billion, down 12% and 22% respectively.

During the period, the company’s gross profit reached 650 billion. Gross profit margin narrowed from 27.5% in the same period to 22.8% this quarter. Financial revenue increased while interest expenses were reduced, and at the same time, there was an additional income from insurance reimbursement of VND 131 billion. As a result, the company reported a profit after tax of VND 396 billion, down 42% compared to the same period last year.

At Gemadept Joint Stock Company (Ticker: GMD), the company recorded a nearly unchanged first quarter net revenue compared to the same period last year. However, net profit decreased by 26% to 202 billion dong, partly due to the profit from Gemadept’s joint ventures and associates which decreased by 83% to 21 billion dong while the same period profit was 126 billion dong. In addition, expenses such as finance and business management increased by 25% and 37%, respectively.

With Hai An Transport and Loading Joint Stock Company (Code: HAH), the business results in the first quarter were not only affected by the decline in freight rates and ship rentals, but also from the upgrade and repair of the yard. Currently, the number of ships of the company has decreased from 11 to 9 in the context of sea freight rates, ship rental prices decline.

In the first quarter, the company recorded net revenue of 655 billion dong, equivalent to the same period last year. However, COGS increased by 48% to 463 billion dong, mainly due to the cost of ship operations, causing gross profit margin to decrease from 52% in the same period to 29% this quarter. Expenses such as finance and corporate management all increased compared to the first quarter of 2022, causing net profit to decrease by 40% to 119 billion dong.

In the oil and gas transportation segment, business results in the first quarter proved to be better in the context that the world oil trade is expected to continue to be active as Europe is looking for an alternative oil and gas supply. for Russia.

Accordingly, Petrovietnam Transportation Corporation (PVTrans, Code: PVT) recorded first quarter net revenue of VND 2,043 billion, a slight increase compared to the same period last year, but profit after tax increased 24% to VND 240 billion thanks to an increase in profit after tax. increase the efficiency of fleet exploitation and improve the efficiency of financial activities.

Or with Pacific Petroleum Transportation Joint Stock Company (PVTrans Pacific, Code: PVP), net revenue in the first quarter was almost unchanged over the same period at 305 billion dong. However, profit after tax increased 3 times to 47 billion dong because the fleet continued to exploit in the international market with good freight rates, while increasing financial income, reducing production and management costs. business management.

Consolidated financial statement data in the first quarter of companies (synthesized in the US)

Consolidated financial statement data in the first quarter of companies (synthesized in the US)

Careful business plan

Although there is a slight divergence in profits among shipping companies, their overall outlook on this year’s business outlook is still quite cautious.

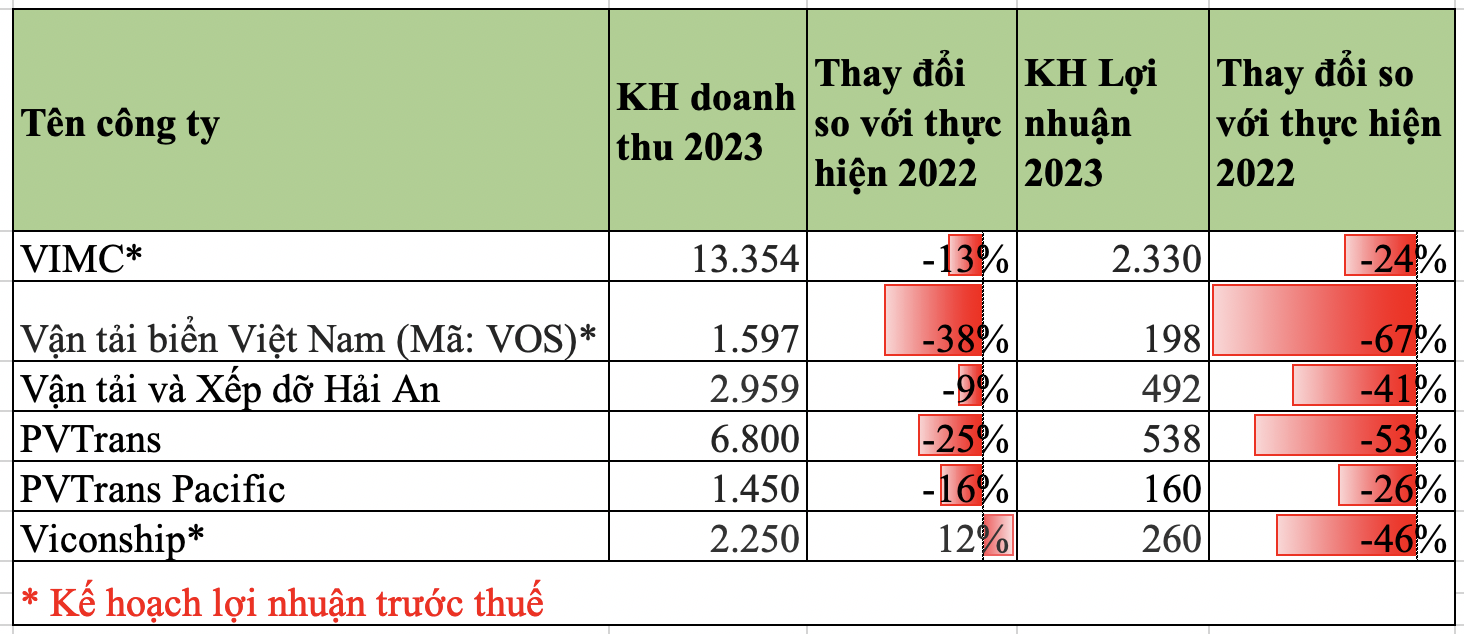

Accordingly, Vietnam National Shipping Lines set a target of 13,354 billion VND in revenue, down 13%, profit before tax is 2,330 billion VND, down 24% over the same period. Mr. Nguyen Canh Tinh – General Director said that before building a plan for 2023 to submit to shareholders, the company considered a lot. Because every shareholder wants profits this year to be higher than last year, but in business there will be ups and downs, not every period is favorable.

“I assess, 2023 is a very difficult year, with more challenges than opportunities, to be profitable is already good. This year, we do not aim to increase profits first, but there are goals that need to be persevered and achieved, such as expanding market share, increasing revenue outside of core activities, “Mr. Tinh. emphasize.

Vietnam Shipping Joint Stock Company (Code: VOS) sets a target that total revenue in 2023 will decrease by 38% to VND 1,597 billion and pre-tax profit will decrease by 67% to VND 198 billion.

With the oil and gas transportation segment, although there were positive signs in the first quarter of the year, businesses also achieved their business goals that were backward compared to 2023.

Typically, PVTrans has a business plan in 2023 with a revenue target of VND 6,800 billion and a profit after tax of VND 538 billion, down 25% and 53% respectively compared to the results of 2022.

Mr. Nguyen Duyen Hieu, Member of the Board of Directors, General Director, said that the international shipping market is forecasted to remain relatively positive in the context of limited supply of ships. However, the outlook could be influenced by risks related to economic growth and OPEC+ oil production cuts. Therefore, freight rates in 2023, will cool down after local growth in 2022.

For the domestic market, fuel consumption demand may be negatively impacted by the risk of slowing economic recovery and high inflation. Therefore, the volume of transporting crude oil, petrol and LPG is not expected to grow strongly compared to 2022.

Besides, the maintenance plan of Dung Quat Oil Refinery has been moved to early 2024 and this year Nghi Son Refinery and Petrochemicals will stop working for about 45-50 days for maintenance.

Source: Minutes and documents of the General Meeting of Shareholders of companies in 2023 (collected by the US)

Can the shipping industry recover from the third quarter?

The decline in sea freight rates is expected to slow down and bottom in the second quarter and recover from the third quarter of this year.

“I think the shipping industry can recover in the third quarter, in which the biggest catalyst comes from the Chinese market, when the country increases trade after the opening period. I think the market may recover in a V-shape. The second quarter will be the time to create a bottom,” said Mr. Trung.

According to Mr. Trung, the transportation industry cycle also operates according to the economic cycle, and the reduction in freight rates and services will only happen in a short time and the market will have many new opportunities.

“We are focusing on investing heavily in technology innovation, fleet, equipment status, infrastructure, investment in people and finally pushing into digital transformation,” Trung said.

In the period of 2021 – 2025, the company said it will liquidate 24 ships with a total tonnage of about 617,000 tons (DWT), of which, in 2023 alone, it will sell 9 ships. In addition, the company invests in 4 container ships from 1,700 to 2,200 TEUs and 8 dry cargo ships with a tonnage of up to 60,000 tons (DWT).

It is expected that by 2025, VIMC’s fleet will have a total of 40 ships with a total tonnage of about 1.2 million tons. In which, the container fleet has a tonnage of about 200,000 tons DWT (13,000 – 16,000 TEU), equivalent to 30% of the tonnage of Vietnam’s container fleet.

“The liquidation of old ships is partly because the repair costs are too high and the ships do not meet the environmental conventions to enter some ports. In addition, the money from the liquidation of the ship will help us reinvest,” said Trung.

Some other companies are taking advantage of the falling market to carry out mergers and acquisitions (M&A) deals, preparing for a long race.

For example, Container Group JSC (Viconship, code VSC) recently approved a plan to issue more than 121 million shares at a ratio of 1:1 to existing shareholders at the price of 10,000 VND/share.

If successful, the amount will be about 1,213 billion VND; in which the company used 1,200 billion dong to invest in controlling 1 enterprise in the seaport sector based in Hai Phong city through capital transfer. Total expected investment capital in this company is 2,250 billion VND. The remaining capital (1,050 billion VND) is expected to be proactively mobilized by the company and mobilized from credit groups and businesses.

Talking to us on the sidelines of a logistics industry event held on May 11, Mr. Cap Trong Cuong, General Director of Vicoship said that this deal is to anticipate the trend in the near future and at the same time expand the scale of production. .

Mr. Cap Trong Cuong, General Director of Vicoship (Photo: H.My)

He also believes that by the third quarter at the latest, Vietnam’s shipping industry will recover. However, he did not expect a boom.

“I do not expect the transport market and seaport services to boom again like in the past. Anything that spikes is not good either. If we have a steady growth, there is accumulation much better. This will help computational administrators not fall into a passive state,” said Mr. Cuong.

Sharing with us, Mr. Priskoka Aleksandr – Deputy Director of Commercial and Business Development in Asia, Fesco Shipping Group – one of Russia’s largest shipping carriers, said that the market situation will warm up starting beginning in the second quarter.

Mr. Priskoka Aleksandr – Deputy Director of Commercial and Business Development in Asia, Fesco Transport Group (Photo: H.A.)

“The sharp drop in freight rates recently, especially in February and March, is normal and cyclical when the demand for transportation in markets, especially in Asia is at a low stage. This is nothing to worry about. I think the shipping market situation will warm up from the second quarter and we are preparing for this,” he said.

According to VietnamBIz.vn