The Logistics Industry Update Report has just been released, SSI Research said, becoming more severe congestion and disruption has pushed freight rates to record highs. Container freight rates have increased four times the pre-epidemic level.

WHAT INDUSTRY BENEFITS, WHAT INDUSTRY DAMAGE?

Specifically, freight rates are higher on long-haul routes, such as Asia-Europe and Asia-North America. Freight charges at these routes have increased about 4 to 8 times within a year. On the other hand, fares for short-haul or intra-regional routes increased more modestly.

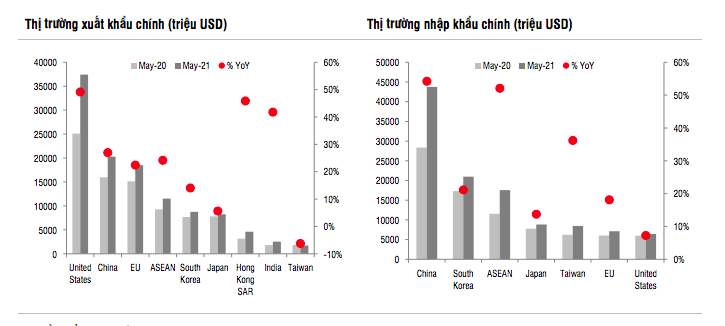

Exports from Vietnam to Europe and North America were hardest hit, while imports from these markets and intra-Asia shipping were also affected but to a lesser extent.

The Covid-19 epidemic is the main cause of the increase in container shipping costs since 2020. Shipping companies have made large-scale reductions in capacity, severe port congestion, and imbalance. Increased trade, empty container shortages and some major ports partially closed.

Besides, a number of factors lead to high freight rates in the long term such as: Higher fuel costs, the trend of increasing container ship sizes, and the influence of maritime alliances.

Vietnam is not involved in intercontinental shipping, so Vietnamese businesses are generally negatively affected by the increase in freight rates on long routes.

In the Asian market, Vietnam has a number of shipping companies operating on a very limited scale, so the positive impact is there but not much. Overall, however, profit growth was very positive, up 106% y/y thanks to strong import/export activities and growing demand for logistics services such as warehousing or internal transportation. geography.

For mixed logistics companies (warehouse, depot, ICD, etc.), there was a strong improvement in both revenue and net profit (+87% and 62% y/y respectively). This could be due to: Good growth in export/import activities; The demand for storage increases when there is a shortage of containers; and higher freight rates due to increased demand.

Improvement was also seen in port companies with revenue growth of 13% and profit growth of 37% yoy.

For exporting companies, most incur additional shipping costs either partially or completely, regardless of FOB or CIF terms.

Shipping costs to US/European markets have increased 2-3 times in the past year. Most companies in Vietnam import under CIF terms and export on FOB terms. Companies that export on FOB terms do not incur direct freight charges but must share in the increased shipping costs by reducing the average selling price.

As a result, import/export companies with a high import-export ratio to the US/European markets will experience lower average selling prices/profit margins due to this effect. The hardest hit are low-value commodity sectors like fisheries and agriculture.

WHEN DOES THE RATE REVERSE?

According to SSI Research, there are currently many factors affecting the shipping market. It is difficult to say exactly how much impact each factor has on this condition. But some factors are only temporary and will inevitably reverse in due course, while others are quite long-term and won’t change anytime soon. This suggests that an escalation of short-term factors could push freight rates to new highs, such high rates will not be sustainable in the long term.

Specifically, a number of short-term factors that may gradually decrease in the near future are as follows: Post-epidemic pent up demand and increased inventory import activity in North America/Europe: Normally, there are two peak export seasons. from Asia to North America/Europe, it’s July (back to school season) and October (Christmas season). Currently, some airlines have started to apply peak season surcharges for these service routes. This is the strongest short-term driver of the rate hikes, and this won’t end until the end of 2021.

Social distancing and congestion at Chinese ports: Recent events in Yan Tian and Kaohsiung (Kaohsiung) ports are likely to be under control in a few weeks. Similar to the Suez Canal event, these local events put enormous pressure on the global supply chain and can take several months to resolve these bottlenecks.

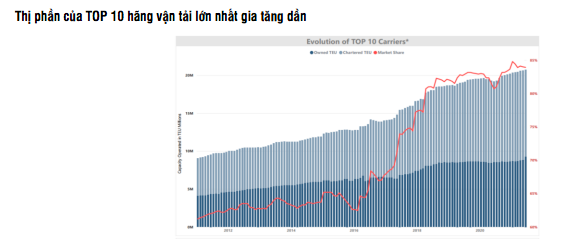

In the long term, the following factors can exist and keep freight rates higher than the pre-Covid-19 average: Strengthening cooperation in controlling supply and prices between carriers due to the formation more alliances and M&A in recent years; The trend of increasing ship size makes supply chain management less flexible and increases costs when faults occur; A higher rate of long-term contracts can keep rates more stable, but at a higher rate.

“In summary, freight rates may peak in the fourth quarter of 2021, then adjust slightly in the first half of 2022. Rates may decrease significantly in 2023 when the new supply of ships comes into operation, but only maintained at a higher level than before the Covid epidemic. According to Drewry, average freight rates may increase by 23% this year and may decrease slightly by about 9% in 2022 as demand returns to normal, while long-term rates are expected to remain higher than pre-epidemic levels. Covid-19, as carriers have more experience in supply management and increased cooperation,” emphasized SSI Research.

According to VnEconomy