Container freight rates are showing signs of cooling amid falling demand while vessel and container capacity is being replenished.

According toThe Load Star, There is more evidence in the container port freight market this week that ocean container rates on many routes have peaked.

All three major indexes tracking shipping rates recorded single-digit declines due to a drop in cargo handling in Asia.

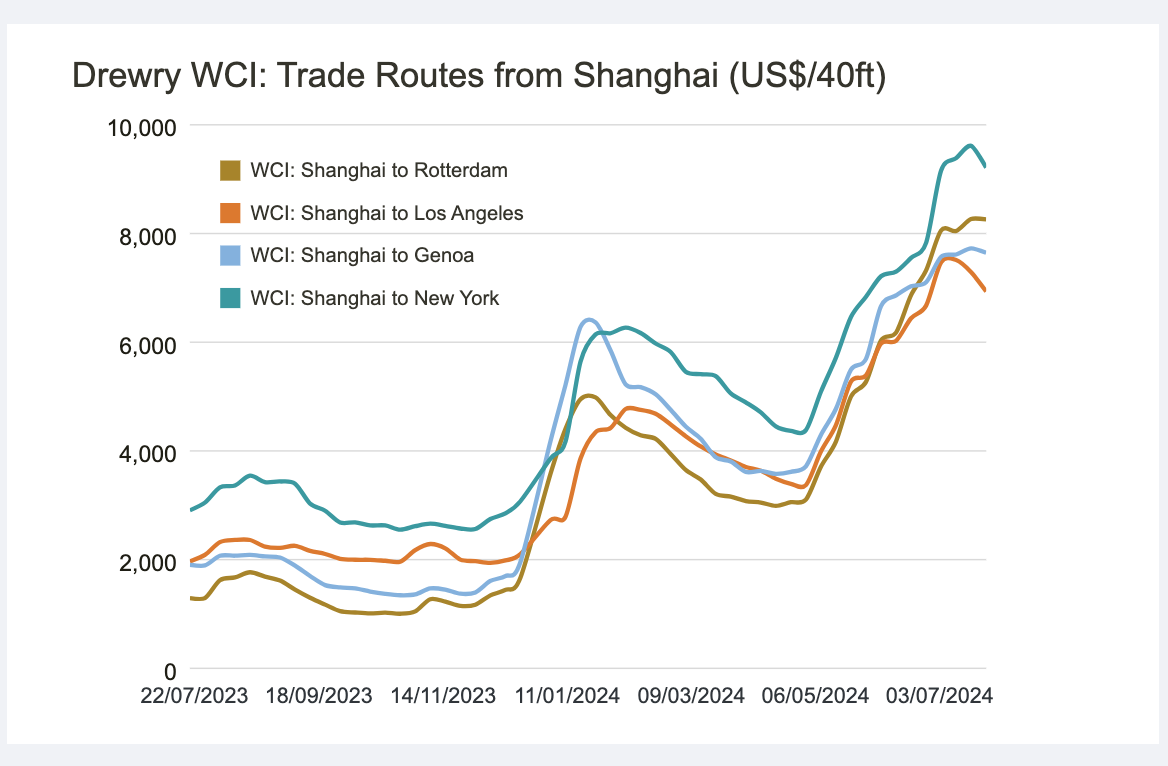

The sharpest declines were recorded on the trans-Pacific trade from Asia to North America, with Drewry’s World Container Rate Index (WCI) from Shanghai to Los Angeles falling 5% week-on-week to $6,934 per 40-foot container.

World Container Freight Index (WCI) Developments (Source: Drewry)

The XSI index, which tracks contract rates developed by rate consultancy Xeneta, fell 6% to $7,322 per FEU.

The FBX index of international shipping booking and payment platform Freightos fell 4% to $7,738 per FEU.

Meanwhile, rates on the Asia-North Europe trade were either stable or slightly down. WCI and XSI were stable at $8,260 and $8,474 per FEU, respectively.

Asia-Europe freight forwarding sources confirm that bookings have become easier over the past two weeks, suggesting that demand has started to ease or that the massive capacity additions since the start of the year are finally starting to pay off.

“It has definitely become easier to find space in the last two weeks, although we still have to stick to the allocation and anything above that has to go to spot/FAK,” said one forwarder.

WCI’s Shanghai-Genoa spot rate fell 1% to close at $7,645/FEU, while FBX’s Asia-Mediterranean rate fell 3% week-on-week to $7,508/FEU.

Container shipping rates from Shanghai to Europe, America (Source: Drewry)

According to data from Alphaliner this week, every major carrier – except Yang Ming – saw capacity increase in the first half of the year, with MSC leading the way, adding around 400,000 TEUs (20-foot containers) to its fleet since January. The total capacity of the MSC fleet now stands at more than 6 million TEUs.

In addition, both MSC and CMA CGM have around 1.2 million TEUs of capacity on order this year and next. Alphaliner notes that there is a “strong possibility” that the French carrier will overtake Maersk as the second-largest carrier within the next two to three years.

Meanwhile, falling spot freight rates have ended more than three months of increases and are starting to affect the charter market, with the Hamburg and Bremen Shipbrokers’ Association (VHBS) noting this week that carriers are becoming more cautious in negotiations with shipowners.

“This caution is justified, given the weakness in spot freight rates; the freight index,” wrote VHBS director Alexander Geisler. export Shanghai Container Lines (SCFI) posted its second weekly decline last Friday, after 13 consecutive weeks of gains.”

The continued increase in new shipbuilding capacity is gradually eroding the current solid foundation of the market, he added. freight The decline could come earlier than expected this year, as the early start of the peak season will test the market’s resilience to a glut of new vessels.

With more than 1.3 million teu of new ships yet to be delivered by the end of this year and a further 2 million teu by 2025, there could be some tumultuous times ahead for owners and operators.

According to VietnamBiz.vn