Source: dttc.sggp.org.vn

Raw material demand decreases in 2023

The latest December 2023 report from the US Department of Agriculture shows that total global powdered milk production in 2023 is estimated to reach 9.2 million tons, including 4.4 million tons of whole milk powder and 4.8 million tons of milk powder. Skimmed milk powder. The output figure barely increases compared to 2022. However, the total domestic demand for milk powder of countries in 2023 is estimated to decrease by 3.1%.

Therefore, the demand for imported milk powder is estimated to only reach 2.5 million tons, equivalent to a decrease of 8% compared to 2022. The reason for the decrease in import demand is that China shows strong growth (nearly 12%) in domestic production of whole milk powder, so China’s need to import this type of milk powder in 2023 will decrease by 36% compared to 2022. Meanwhile, for skimmed milk powder, the EU’s consumption demand will decrease by 36% compared to 2022. (largest consuming area) decreased by 12.4% due to stagnant economic growth.

As of December 27, 2023, the latest futures contract for whole milk powder on the NZX (New Zealand) was trading around 3,245 USD/ton, down 15.6% compared to the peak of 3,845 USD/ton. established in March 2022. Similarly, the price of skim milk powder on CME also decreased by 34.9% in the same period, trading around 119.2 cents/pound in the last week of December 2023.

Milk output is expected to increase from mid-2024 thanks to the increasing trend of milk powder prices since August 2023, which is a positive factor for the profits of Vietnam’s dairy industry.

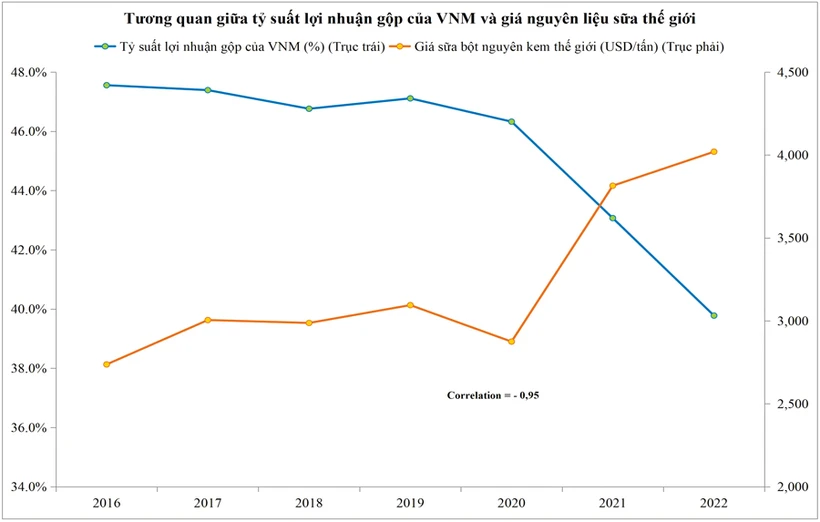

Milk raw material prices have a very high negative correlation with the gross profit margin of dairy companies. On average, the price of whole milk powder in 2023 is about 27.7% lower than the average in 2022. From there, the gross profit margin in the first 3 quarters of this year of Vietnam Dairy Products Joint Stock Company (VNM) and Joint Stock Company International Dairy (IDP) increased slightly compared to 2022.

Prospects for raw material prices in 2024

New Zealand’s whole milk powder production is forecast to decrease to only 1.33 million tons in 2024, down 5.4% compared to 2023 due to lower milk supply (reduced number of dairy cows) and lower profits. for the production of this item compared to other products.

The world’s total production of whole milk powder in 2024 is also forecast to decrease by 0.6% compared to 2023, but will be 0.8% higher than in 2022. Meanwhile, skimmed milk powder is forecast to production increased sharply by 3.4% with global output likely to reach 4.96 million tons, thanks to an 8.9% increase in US production.

The US export position for this product is also forecast to surpass the EU in 2024 thanks to its price advantage, when comparing the FOB price in the US market of about 1.21 cents/pound and the EU market of about 1.21 cents/pound. 36 cents/pound.

The balance of supply and demand in 2024 is expected to tilt towards surplus, when the US Department of Agriculture forecasts that total milk powder production in 2024 will increase by 138,000 tons, an increase of about 1.5% compared to 2023 output. Meanwhile, demand Consumption demand is also forecast to increase by 101,000 tons. However, import demand is forecast to decrease due to the trend of domestic product consumption.

Accordingly, import demand is forecast to be only about 2.49 million tons, down 1.1% compared to 2023. Although total powdered milk production in 2024 is still forecast to increase, Rabobank (specializing in agricultural consulting forecast), assesses that output in the first quarter of 2024 is likely to decrease due to the low milk price trend in the first half of 2023, which has made upstream profit margins negative, leading to farmers being forced to must cut costs and eliminate cows with low profit margins. But output is expected to increase from mid-2024 onwards, thanks to the upward trend in powdered milk prices since August 2023 until now.

In addition, an additional factor supporting the downward trend of raw milk prices is that the price trend of agricultural products and animal feed is also forecast to decrease due to abundant harvest output. Corn prices for the 2023-2024 season could decrease by more than 160 cents/bushel compared to the average level of the 2022-2023 season.

The medium-term trend of corn prices will also decrease by nearly 50 cents/bushel in the next crop season 2024-2025 due to the trend of crop expansion, ending inventories are forecast to increase and weigh on corn prices. Soybean meal prices are also forecast to decrease sharply in the near future thanks to the expected large surplus harvest output.

The supply-demand balance could widen to a surplus if demand is actually affected by the economic soft landing, as expected by major central banks. With high milk prices, while other broader cost of living issues are causing headaches for people in developed countries, as shown by the CPI index having increased for nearly 3 years.

Weak consumer confidence is expected to be imminent. The risk to the economy is that if there is a sharp drop in prices in the asset market, it could have a major impact on consumer psychology, affect money supply and increase unemployment in 2024.

However, if the economy only has a soft landing without an accompanying decline in asset markets, stable demand could help reduce raw milk prices amid increased production on the supply side.

That is expected to help increase gross profit margins of domestic dairy enterprises. The fact that the economy only had a soft landing helped stabilize revenue, leading to positive expectations for the industry’s profits.